No matter the industry, and no matter how healthy the business looks today, three board conversations show up sooner or later.

A number gets missed. Cash stops feeling comfortable. Or someone finally says the quiet part out loud: the strategy on paper is not matching reality in the business.

The difference between a CFO who feels calm and a CFO who feels constantly on defense is not IQ. It’s preparation.

As I shared in my solo episode “What I’ve Realized After Six Months as CFO” on The Diary of a CFO, the pressure isn’t the deck, it’s the seat. In a board meeting, directors aren’t only listening to your update. Every time you open your mouth, they’re assessing whether you’re the right person for the situation the company is in.

That’s why you should pre-game these conversations before they happen by building a simple structure you can reuse.

This article breaks down the three conversations and gives you a practical playbook for each.

Key takeaways

The three inevitable board conversations for a new CFO are missed numbers, cash runway, and strategy reality checks.

You can prepare for all three using one reusable structure: Headline → Facts → Cause → What changed → Plan → Ask → Risk view.

The goal is to avoid surprise, tell the truth early, and keep the board focused on decisions instead of blame.

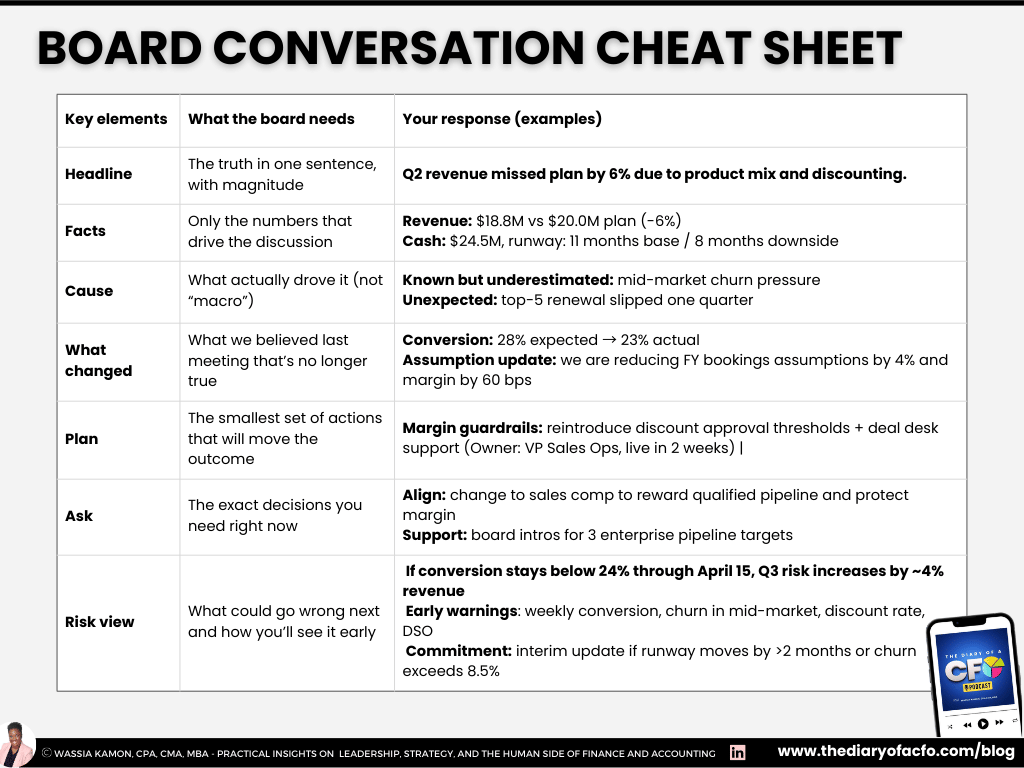

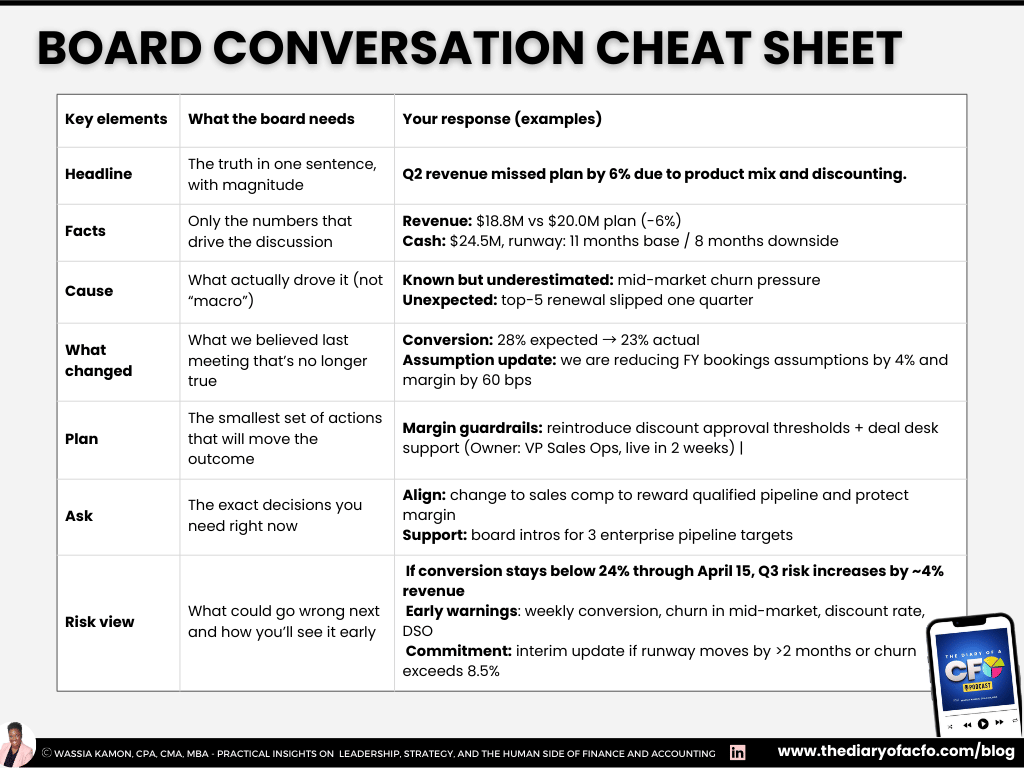

The reusable structure for all three board conversations

Before we get into each scenario, here is a structure you can reuse for almost any tough board conversation:

Headline

One sentence, plain language, no defensiveness. “What is going on.”Facts

Three to five bullets of facts. No data dump. Details live in the appendix.Cause

The real drivers. Separate what was known, what was a surprise, and what was execution.What changed

What you believed last time that is no longer true.Plan

Concrete actions with owners and timing.Ask

What decision or support you need from the board.Risk view

What could go wrong next, and how you will see it sooner.

You can literally keep this as a checklist next to your keyboard when you write your board narrative.

Board Meeting Prep Template for CFOs

How should a CFO communicate with the board when numbers are missed?

Short answer: Lead with the miss and magnitude, name the 2–3 real drivers, explain what changed since the last forecast, and present 2–3 corrective actions with owners and timing, then ask the board to approve the updated outlook or the specific change you need.

Here is how it would like using our 7 steps:

Headline

“Q2 revenue came in 6 percent below plan, and gross margin was 120 basis points lower than what we shared at the last board meeting.”

Facts

Revenue: 18.8 million versus 20.0 million plan (–6 percent)

Gross margin: 41.3 percent versus 42.5 percent plan (–120 bps)

EBITDA: 1.1 million versus 2.0 million plan (–0.9 million)

Cash: 24.5 million; runway 11 months base, 8 months downside

Cause

Known but underestimated: mid‑market churn pressure that slipped one quarter

Unexpected: a top‑five renewal pushed out and a competitor promo in a core region

Execution: discount discipline slipped in two regions; sales cycle lengthened by 10 days

On “Balancing Strategy, Risk and Leadership as a CFO,” Scott Meyers made the point that bad news is where your communication really gets tested. He said your speed and calm matter when you are giving bad news, because the faster you share it, the more time people have to react.

What changed

Conversion: 28 percent expected → 23 percent actual

Cycle time: 52 days → 62 days

Churn (mid‑market): 6.2 percent → 8.1 percent

Assumptions: you are reducing full‑year bookings assumptions by 4 percent and margin by 60 bps

You are explicitly saying, “The model now reflects what actually happened.”

Plan

Pipeline truth cadence: weekly “commit criteria” review, owned by the CRO, starting next Monday

Margin guardrails: reintroduce discount approval thresholds and add deal review support from sales ops within two weeks

Retention response: top‑20 at‑risk accounts get an executive‑sponsored playbook, owned by the customer success lead, live in three weeks

Three moves, each with an owner and a timeline. Not a 20‑point wish list.

Ask

Approve a revised full‑year outlook and updated operating plan based on the new assumptions

Align on a change to sales compensation to reward qualified pipeline and protect margin

Optional: support intros to three enterprise prospects where board relationships can move deals forward

Risk view

Downside: if conversion stays below 24 percent through April 15, Q3 revenue will be about 4 percent lower than current plan

Early warnings: weekly conversion in late‑stage pipeline, churn in mid‑market, discount rate, and DSO

Commitment: you will send an interim update if runway moves by more than two months or churn exceeds a defined threshold

What a missed‑numbers conversation can sound like in practice

Let's say you are a few quarters into the role, and the first real miss lands on your watch.

Instead of waiting for the board pack to go out, schedule a short call with your board chair and audit chair. Open with the headline: “We missed Q2 revenue by 6 percent and margin by 120 bps. Let me walk you through why and what we’re already doing.”

By the time you get to the board meeting, the miss is not a surprise. The conversation moves quickly to your plan and the ask, which is exactly what Scott meant when he said:

Board meetings should feel more like a formality than a reveal.

You can listen to the full conversation with Scott here:

Balancing Strategy, Risk & Leadership as a CFO, with Scott Meyers

How do you present cash runway to the board without panic?

State runway in base and downside cases, explain the drivers of burn and working capital, present the concrete levers to extend runway (cost, collections, pacing), and ask the board to approve the immediate actions and agree on the trigger point for funding.

Here is how it would like using our 7 steps:

Headline

“At our current burn, we have 11 months of cash runway. In a reasonable downside, that drops to 8 months. With the actions we are proposing, we can extend runway to about 14 months.”

Facts

Cash on hand: 24.5 million

Base case burn: 2.2 million per month

Base case runway: 11 months

Downside runway (10 percent lower bookings): 8 months

Runway with actions: 14 months

Cause

Revenue: bookings in mid‑market have been 10 percent below plan for two quarters

Costs: go‑to‑market and product headcount grew ahead of revenue; capex for a major project ran 20 percent over budget

Working capital: DSO increased from 45 to 58 days; inventory is 18 percent over target

Scott talked about this kind of moment very directly. He said that as CFO, you are often the first to see that something is existential, and that it is hard to be the first one who sees the trouble on the horizon.

What changed

Previous belief: bookings of 7 million per quarter and DSO of 45 days

Current reality: bookings at 6.3 million and DSO at 58 days

Previous belief: a credit line increase by Q4

Current reality: lender timelines have moved out by at least one to two quarters

Plan

Reduce burn: pause hiring in non‑critical G&A, slow discretionary marketing, and phase the capex project into two stages

Improve working capital: tighten payment terms on new contracts, implement a focused collections sprint on top 30 accounts, and work down slow‑moving inventory

Prepare funding: refresh your lender and investor materials and start informal conversations, so you are not starting from zero if you need to raise

Scott used a simple image for this mindset: if the house is on fire, you want to know where the fire extinguisher is, use it, and then fix the wiring. This plan covers all three.

Ask

Approve phase one cost actions that reduce burn by 400 thousand per month starting next month

Approve a temporary hiring pause outside of revenue‑generating roles until runway is back above 12 months

Align on a threshold (for example, 9 months of runway) that will trigger a formal decision to pursue funding

Risk view

If bookings stay at current levels and actions are delayed, runway falls below 6 months by the end of Q1 next year

If only half of the cost plan is executed, you will likely need external funding by the end of Q4 in the downside case

You will monitor bookings, burn, and DSO weekly and send a short update if projected runway moves by more than two months

How to pre-game a cash runway conversation

Call your CEO and walk through the seven steps until you are aligned. Then you set up brief calls with your board chair and your finance committee lead. Clearly say: “I want to give you a clear view of cash before our next meeting. At our current burn, runway is 11 months. If bookings stay soft, it drops to 8. If we pull the actions I’m recommending, we can extend it to about 14. Here’s how.”

You give them the facts and the plan before they ever see the deck. By the time the full board meets, people have had time to absorb the tradeoffs. The question in the room is not “Are we in trouble” but “Which mix of cost, working capital, and funding are we comfortable with right now.”

How do you reset a strategy with the board when reality changes?

When strategy isn’t matching reality. say clearly what part of the strategy is no longer achievable as written, show the constraint (capacity, timeline, economics), propose a focused revised plan (what we will do, what we will stop, and the new targets), then ask the board to approve the reset and align on tradeoffs.

Here is how it would like using our 7 steps:

Headline

“With our current capacity and constraints, we cannot deliver the original three‑year strategy as written. Here is what we can realistically deliver, and what needs to change.”

Facts

Original plan: grow revenue 20 percent per year, launch a new product in Q2 next year, and lift margin to 45 percent over three years

Actual to date: revenue growing at 11–12 percent; product launch running six months late; margin at 40 percent and flat

Execution strain: key roles in product and data unfilled; implementation cycles 30 percent longer than planned; teams running eight major initiatives in parallel

Cause

Internal: hiring for specialised roles is slower; core systems and processes are not ready for the volume of change; too many big projects running at the same time

External: demand in one target segment has softened; regulatory requirements added complexity to the new product; competitors responded faster than expected in another region

In “The Art of Becoming a Strategic CFO, with Dr Tamer Alsayed,” we discussed this exact tension. Tamer described a strategic CFO as the person who bridges vision and execution and who keeps the strategy honest without being purely pessimistic.

What changed

Previous assumption: ramp time of three months for key roles and implementation cycles of eight weeks

Current reality: ramp closer to five months and cycles at eleven to twelve weeks

Previous assumption: the organisation could run eight major strategic initiatives at once

Current reality: quality and speed drop when more than four are live at the same time

You are not blaming anyone; you are telling the truth about capacity.

Plan

Focus: reduce major initiatives from eight to four; put the lowest‑impact projects on hold

Timeline: extend the new product launch by six months, and rebaseline key milestones and customer commitments

Resources: move talent and budget from paused initiatives into the top three priorities; fill the two or three key roles before adding new projects

Narrative: update the external story so it reflects a focused, credible set of bets instead of a long wish list

Tamer shared a practical trick for this kind of board update. He often starts with one slide that shows what happened, what is challenging, the critical numbers, and his recommendation. He said that most of the time the board stays on that one slide because it tells the story without fluff.

Ask

Approve a tighter version of the strategy focused on four core initiatives instead of eight

Approve updated revenue and margin targets and a revised three‑year plan that reflects actual capacity and current market conditions

Align on which initiatives and experiments will be stopped so that people and budget can move to the priorities you just agreed on

Risk view

If you keep pushing the original strategy as written, you risk repeated execution misses, team burnout, and erosion of credibility with the board and external stakeholders

If you adjust now but do not enforce focus, you risk sliding back into “everything is a priority” within a year

You will track a small set of indicators on execution capacity and strategy progress and bring a focused update back to the board in six months

What a strategy reset conversation can sound like in practice

Using the seven‑part structure, you can build a single executive summary slide for the biggest initiative that is off track have separate prep meetings with the CEO and board / committee chair to go over it and get early alignment.

This way, by the time you reach the full board session, the conversation is not a public ambush of the strategy. It is a joint decision on where to focus, anchored in a simple, honest narrative that feels like it came from a CFO who understands both the numbers and the reality on the ground.

Bringing it all together

If you only remember one thing from this article, let it be this: the board is not grading you on perfection, they are grading you on preparation. Missed numbers, cash pressure, and strategy drift are part of running a real company. What separates trusted CFOs from anxious ones is whether those conversations feel structured and early or chaotic and late.

If you use the same simple checklist every time you brief the board, you make those moments a lot less dramatic. You show up with a clear headline, the few facts that matter, a real explanation, and a plan with owners, timing, and risks. You stop treating the board meeting as a performance and start treating it as a working session with partners.

You will not control everything that happens in the business. But you can control how you talk about it. And for a new CFO, that is often the difference between being seen as “the person who owns the numbers” and being seen as a peer who can help the board steer through whatever comes next.

Episodes to go deeper on these conversations

If you want to go deeper into these three board conversations, these episodes of The Diary of a CFO are a good next step:

What I’ve Realized After Six Months as CFO

My early lessons from the first six months in the role, including what surprised me about board dynamics and why dealing with a board as a CFO is very different from preparing slides.Balancing Strategy, Risk & Leadership as a CFO, with Scott Meyers

A practical conversation about no‑surprise board meetings, how to deliver bad news with speed and calm, and what it feels like to be the first person to see trouble on the horizon.The Art of Becoming a Strategic CFO, with Dr Tamer Alsayed

How to think like a strategic CFO, use simple one‑slide narratives with your board, and reset strategy without losing credibility.

Board Meeting Prep FAQ for New CFOs

What should a new CFO say first when numbers are missed?

Start with one sentence: the miss, the magnitude, and the key driver—no defensiveness.

How much detail does a board want on cash runway?

The board wants the runway range, assumptions, downside case, and the decision needed—details can live in backup.

What’s the simplest structure for any CFO board update?

Headline → Facts → Cause → What changed → Plan → Ask → Risk view.

How should a new CFO prepare for their first board meeting?

Start by understanding the board’s priorities and personalities, not just the numbers. In “What I’ve Realized After Six Months as CFO,” I talked about how every board member hears the same message differently. Some care more about risk, others about growth, some only want the big picture.

Review the last two or three board packs, talk with the CEO and board chair about what people really care about, and then use the 7-part structure to shape your story around those priorities.

How often should a CFO talk to the board outside of board meetings?

More than you think. Scott Meyers pointed out that your “board meetings really happen kind of outside of the meetings,” and that you should be conversing with your board so there are no surprises.

For most new CFOs, that means regular conversations with the CEO, the board chair, and key committee leads between formal meetings, especially around missed numbers, cash, and strategy.

How honest should a CFO be about missed numbers and cash issues?

You can never be too honest, but you can definitely be under-prepared. Your job is to bring bad news early, explain the drivers in plain language, and outline concrete options. In Scott’s words, you need both speed and calm when you deliver bad news, because that gives the board time to react instead of just react emotionally.

What is the biggest mistake new CFOs make with board communication?

One big mistake is thinking that board work is about slides, not conversations. In my six-month episode, I said that preparing slides is just the tip of the iceberg, and that you only really understand board dynamics once you are in the seat and dealing with the meetings before the meeting and the calls after.

The second mistake is waiting until the board meeting to surface hard issues. If you pre game the three conversations in this article, you will feel very different walking into your next board meeting.

About The Author:

Wassia Kamon is a CFO and the host of The Diary of a CFO, where she interviews finance and business leaders on strategy, risk, and leadership. She writes about finance leadership and governance in small and mid-sized organizations, including what works, what breaks, and how leaders manage growth and complexity without burning out.